Project Crypto

It’s been a while since I wrote about the[SEC’s Project Crypto](get involved(https://philbak.substack.com/p/sec-investor-advisory-committee-speech).

It is easy to submit a comment letter to the SEC, and it is important for individuals and smaller firms to do that, because otherwise the interests of the well-funded and well-lobbied will drown you out.[Here is the link](https://www.sec.gov/about/crypto-task-force/submit-written-input#no-back).

While we are on the topic, I’ll use this opportunity to share one of my favorite things that I’ve ever written - a[comment letter addressing Finra’s 2022 efforts to label non-vanilla ETFs as “complex”](https://philbak.substack.com/p/what-finra-calls-complexity-i-call).

Anyway, the SEC does a great job soliciting public feedback, and they use that feedback to shape their decisions. So it is important to comment, and it is important to track their comments.

I recently put all 251 public comment letters into a dedicated Google Notebook LM, and made that tool available to paid subscribers. It is incredible technology that allows you to run all sorts of analysis on the nature and direction of the comment letters. I’ll share some of the findings for the rest of you freeloaders here.

Keep in mind that most of my queries are biased by my own experience, and related to the tokenization of RWAs and real estate (where I am going), and ETFs (where I am coming from). If you have a different focus, email me for the link for your own precision prompting.

NOTE: the rest of this post was AI generated, using the customized LM and public comment letters as source material, and following dozens of prompt refinements.

The following dossier provides a comprehensive report on the issues, chronological trends, and future trajectory of crypto asset regulation, drawing heavily on comment letters from influential firms.

DOSSIER SECTION 1: EXCHANGE-TRADED PRODUCTS (ETPs) / ETFs

This section summarizes issues and trends related to the structuring, approval, and management of crypto asset-based ETPs, with significant weight given to input from major asset managers and exchanges.

### A. Chronological Trend: From Restriction to Standardization (2024–2025)

Prior Restrictive Stance (Pre-2025):

The SEC historically appliedunique, heightened standardsto crypto ETPs, such as demanding comprehensive surveillance-sharing agreements (SSAs) with regulated markets of “significant size”.

This approach was criticized by Coinbase for creating“brand new tests”untethered from statutory requirements.

Initial approvals for spot Bitcoin and Ether ETPs requiredcash-only creation and redemption, a severe limitation compared to other commodity ETPs.

Approved Ether ETPs were initiallyprohibited from stakingthe underlying assets.

Shift to Expansion and Efficiency (2025 Onward):

Following the shift in regulatory philosophy, ETP applications for assets beyond BTC and ETH, such asSolana (SOL) and XRP, quickly came under consideration.

Issuers began filingamended proposals to permit stakingfor Ether ETPs and new applications explicitly included staking requests for PoS assets like SOL.

The SEC staff issued guidance allowing broker-dealers to facilitatein-kind subscriptions and redemptionsfor crypto asset ETPs, reflecting a move toward industry-standard efficiency.

### B. Core Issues Raised by Influential Commenters

Approval Standards and Credibility:

Coinbase urged the Commission to adopt“a clear set of standards”that are known and knowable to all market participants.

Nasdaq recommended creating aconsistent regulatory frameworkfor ETPs (1933 Act) and ETFs (1940 Act), focusing analysis on the underlying digital asset itself rather than the fund wrapper.

VanEck, 21Shares, and Canary Capital stressed that the failure to practice the“first-to-file”principle for approvals discouraged innovation and unfairly benefited established, large brands.

Operational Requirements:

CoinShares noted that their successful European digital asset ETPs rely solely onin-kind creation and redemption, arguing this mechanism minimizes friction, costs, and the potential for “slippage”.

Cumberland argued that requiring cash-only transactions imposesunnecessary trading costson issuers and increases the risk oftracking error.

Staking Integration:

CoinShares and Jito Labs asserted that access to staking rewards isessential for investorsin Proof-of-Stake ETPs due to the inflationary nature of PoS networks.

Jito Labs advocated for the use ofLiquid Staking Tokens (LSTs)as the “best and most clearly viable path” to a fully staked ETP, noting LSTs offer capital efficiency and operational resilience.

### C. Direction of Continuation

Rules-Based Approval:The SEC is expected to establish a consistent, objective framework, potentially drawing on criteria like market capitalization and trading volume, to permit thegeneric listing of qualifying spot crypto ETPs.

Full Integration of Yield:The approval of staking features in PoS ETPs is highly likely, with LSTs becoming a standardized, preferred mechanism to offer investors the full economic benefit of the underlying asset.

Operational Efficiency:In-kind creation and redemption will likely become the market standard, increasing efficiency and reducing tracking error, requiring ongoing coordination between the SEC and FINRA to expedite broker-dealer approvals.

* *

DOSSIER SECTION 2: RWAS AND REAL ESTATE TOKENIZATION

This section addresses the challenges, classifications, and systemic risks associated with tokenizing Real-World Assets (RWAs), focusing on real estate.

### A. Core Issues and Stakeholder Attributions

Legal Classification:

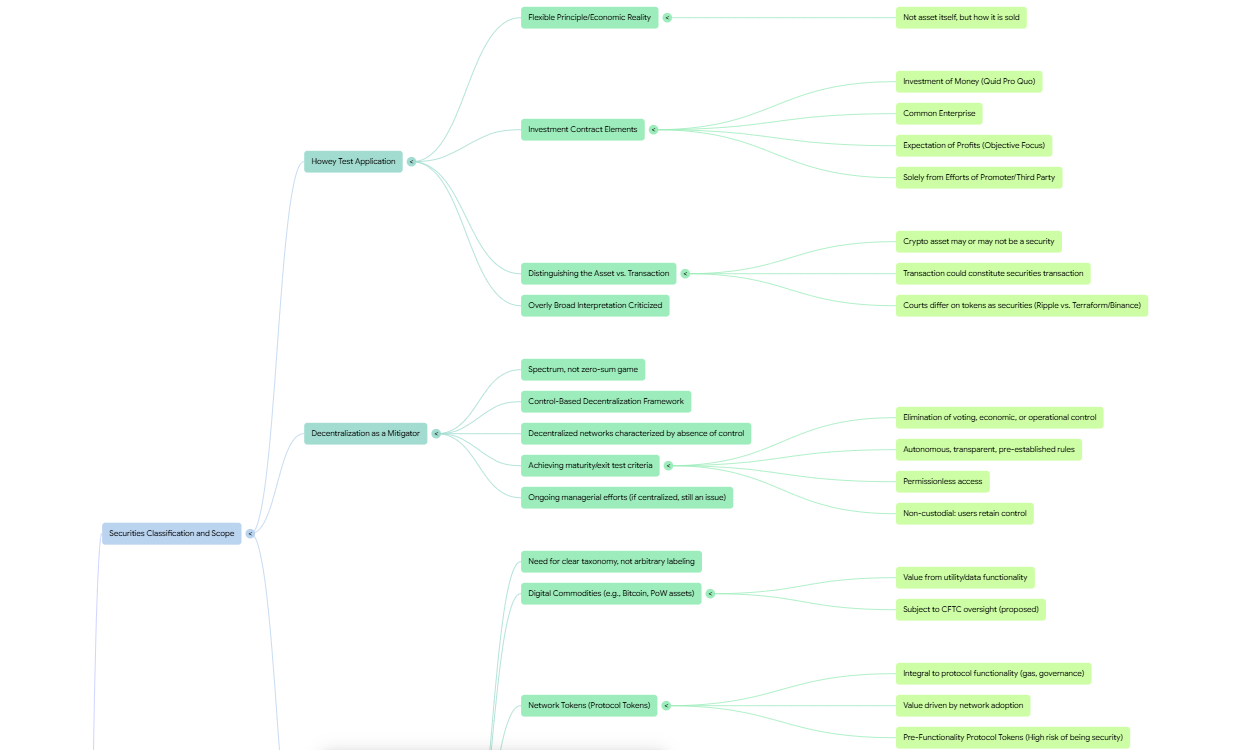

The SEC treatstokenized real estate as securities, specifically as “investment contracts” representing fractional property ownership, building on decades of securities law precedent.

Robinhood affirmed the principle that creating a digital representation of a security“does not change the substance of the security”.

A primary legal issue is defining when tokenized RWAs constitute securities under theHoweyTest, requiring a nuanced taxonomy.

Regulatory Framework Friction:

a16z crypto emphasized that decentralized safe harbors areinappropriate for RWA tokens, as the value of RWA tokens remains inherently tied to centralized, human managerial efforts.

The existingpatchwork of state “blue sky” lawscreates regulatory friction, severely limiting the secondary trading liquidity of tokenized private placements.

Transfer Agent Rules and Efficiency:

Etherealize and Etherfuse identified significant uncertainty regarding whether a crypto network can legally serve as theofficial, authoritative ledger of ownershipfor tokenized securities under current Transfer Agent rules.

SIFMA requested that legacy rules, which require maintaining redundant off-chain records, be modernized to acknowledge that DLT records can be an acceptable alternative.

Technology and Compliance Integration:

Robinhood noted thatprogrammable compliancevia smart contracts (automating AML/KYC, transfer restrictions, and corporate actions) would enhance operational integrity and reduce administrative costs.

Daniel Bruno Corvelo Costa proposed that tokenization frameworks should mandatefull compliance with state property recording statutes(deeds, liens, etc.) and should integrateIoT devicesto provide verifiable physical proof of the RWA’s status and performance.

Market Risk (Citadel):

Citadel Securities warned that unregulated, tokenized “look-a-like” products couldsiphon liquidityaway from established markets and create investor confusion regarding issuer endorsement and counterparty risk.

### B. Critical Monitoring and Trajectory Analysis for a New Real Estate Tokenization Company

A new real estate tokenization company must prioritize monitoring issues that directly impact liquidity and legal standing:

1. Blue Sky Law Resolution:

Crucial Focus:Whether Congress or the SEC establishes afederal preemptionor a workable national standard for secondary trading of tokenized securities issued under Reg A/D.

Trajectory:Likely toward targeted relief or a “sandbox” approach to test solutions, as industry demand for liquidity is immense.

2. Transfer Agent Rule Clarification:

Crucial Focus:Finalizing guidance that recognizes the Distributed Ledger (blockchain) as theMaster Securityholder File.

Trajectory:High likelihood of modernization, as SEC leadership acknowledges legacy rules are stifling tokenization innovation.

3. Howey Test (Efforts of Others):

Crucial Focus:Obtaining clarity on the definition of routine vs. managerial efforts (e.g., differentiating passive rent collection/maintenance from value-adding entrepreneurial activity).

Trajectory:Continued application of theHoweytest, but with growing recognition that tokenization necessitatestechnology-neutral interpretive guidanceon managerial control.

#### Best Case and Worst Case Scenarios for the Real Estate Tokenization Industry

Best Case Scenario:

The SEC issuesclear, coordinated guidanceresolving the conflicts between federal securities law and state property/resale laws. DLT is recognized as a compliant recordkeeping system, resulting insignificant efficiency gains, institutional adoption, and the creation of highly liquid, transparent fractional ownership markets for real estate.

Worst Case Scenario:

Regulatory uncertainty persists, particularly regarding theunresolved burden of state “blue sky” lawsand the need for redundant recordkeeping. Innovation is limited to expensive private placements, failing to achieve the promised liquidity and broad access, allowing foreign jurisdictions to assume leadership in RWA tokenization.

* *

DOSSIER SECTION 3: ALL OTHER ISSUES (Regulatory Structure, Philosophy, and General Markets)

This section covers the shift in regulatory philosophy, governance, custody, and broader market infrastructure challenges.

### A. Chronological Shift in Regulatory Philosophy (2024–2025)

Deregulatory Impulse:Donald Trump’s election initiated the most dramatic philosophical change in governmental regulation in over ninety years, emphasizing reduced regulation and enforcement.

SEC Actions:The SEC, under Chair Paul S. Atkins (2025–), established the Crypto Task Force to address regulatory uncertainty. Immediate actions included:

Dismissing “misguided litigation” and actively considering new ETPs based on non-security digital commodities.

Issuing rapid staff-level statements to “clear the brush” on issues such as meme coins and Proof-of-Work mining activities.

Dissent Against Guidance:Commissioner Caroline A. Crenshaw warned against this rapid deregulatory pace, calling it a“Reckless Game of Regulatory Jenga”.

She argued that the use of staff statements and guidance, rather than formalnotice-and-comment rulemaking, allows the agency to adopt extreme positions without accountability or public scrutiny.

Crenshaw stressed that this approach risksdismantling regulatory foundationsestablished over decades and leaving retail investors vulnerable.

### B. Governance, Custody, and Market Structure

Safe Harbors and Decentralization:

The industry, including a16z crypto, pushed for a regulatorysafe harbor(like Rule 195 or Safe Harbor X) to allow early-stage projects time to achieve sufficientdecentralizationwithout immediate registration under the Securities Act.

This is intended to resolve the “chicken-or-the-egg” paradox where tokens must be broadly distributed to achieve decentralization, but broad distribution risks immediate security classification.

Intermediary Role and Consolidation:

SEC Chair Atkins supported allowing regulated registrants (like broker-dealers) tocustody and trade both securities and non-securities under one roof, arguing it could reduce costs.

This vertical integration model was opposed by Nasdaq, which noted that the existing decentralized structure of traditional securities markets is not a relic but a feature designed to mitigate risk and ensure accountability.

Custody Rules (RIA Focus):

The Blockchain Association noted that the current RIA custody rule creates key challenges regarding whether the RIA or its custodian has appropriate periodic testing to reconcile crypto assets against on-chain data.

Figure Markets suggested thatdecentralized Multi-Party Computation (MPC)could be used to satisfy the role of a qualified custodian by allowing multiple parties to approve transactions and ensure client control.

Inter-Agency Conflict:Lewis Rinaudo Cohen highlighted that thebifurcated U.S. regulatory structure(SEC for securities, CFTC for commodities derivatives)“complicates the regulation of the digital asset sector”, resulting in a pervasive environment where entrepreneurs face constant threats of ambiguous litigation.

Securities Holding Infrastructure:Expert analysis by Charles W. Mooney, Jr. concluded that the existing intermediated securities holding infrastructure (DTCC’s monopoly) is maintained byentrenched interests (broker-dealers and banks)who lack incentives to support material modifications, arguing that reform will require top-down regulatory intervention.

### C. Best Data Points Used in Comment Letters

Market Disruption (Academic):Crypto asset prices showed a swift decline (Negative CARs) of\-6.5%following SEC announcements classifying assets as securities.

RWA Market Valuation:The RWA tokenization market expanded by260% in the first half of 2025, reaching over$23 billion.

RWA Market Projection:The RWA market is projected to reach$30 trillion by 2034(Standard Chartered).

Real Estate Projection:Real estate tokenization is projected to grow from$3.5 billion in 2024 to $19.4 billion by 2033.

Custody Disparity (Cumberland):Broker-dealers holding spot BTC take a100% net capital haircut, compared to only a15% haircutfor the ETP shares that track that same asset.

Regulatory Friction (MiCA):The implementation of MiCA in the E.U. created such significant compliance hurdles that market entry for synthetic dollar issuers has beencapital- and resource-intensive.

Compliance Cost:Annual compliance costs for crypto asset ETPs average betweentwo million and five million dollars annually per product, largely driven by manual processes and regulatory uncertainty.

[](https://substackcdn.com/image/fetch/$s!WYET!,fauto,qauto:good,flprogressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F7af076bc-f692-40eb-b01e-db97ec0460f0_1257x750.png)

[](https://substackcdn.com/image/fetch/$s!xvD7!,fauto,qauto:good,flprogressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fcf697b9d-8d7c-4b01-9d23-d57bc03cb6d21031x781.png)

[](https://substackcdn.com/image/fetch/$s!SpqE!,fauto,qauto:good,flprogressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc9b73573-a427-480f-96bc-443d1e50c7411500x732.png)

[](https://substackcdn.com/image/fetch/$s!YMAQ!,fauto,qauto:good,flprogressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F34825adb-1b61-4830-ac6c-b935204e43b41207x728.png)

[](https://substackcdn.com/image/fetch/$s!-C7L!,fauto,qauto:good,flprogressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F930650f0-ec17-46c5-87be-a9bdae0e00cd1182x558.png)

You can include dynamic values by using placeholders like: https://drewdru.local.press/articles/3ece64d7-673c-425e-b5b7-af1e9101d554, Drew Dru, https://philbak.substack.com/p/project-crypto, drewdru, drewdru, drewdru, drewdru These will automatically be replaced with the actual data when the message is sent.